Regime switching Hidden Markov model#

This example replicates the case study analyzing financial time series, specifically the daily difference in log price data of Google’s stock, referred to as returns \(r_t\).

We’ll assume that at any given time \(t\) the stock’s returns will follow one of two regimes: an independent random walk regime where \(r_t \sim \mathcal{N}(\alpha_1, \sigma^2_1)\) and an autoregressive regime where \(r_t \sim \mathcal{N}(\alpha_2 + \rho r_{t-1}, \sigma_2^2)\). Being on either of the two regimes, \(s_t\in \{0, 1\}\), will depend on the previous time’s regime \(s_{t-1}\), call these probabilities \(p_{s_{t-1}, s_{t}}\) for \(s_{t-1}, s_t \in \{0, 1\}\). Set as parameters of the model \(p_{1,1}\) and \(p_{2,2}\) and define the complementary probabilities by definition: \(p_{1,2} = 1-p_{1,1}\) and \(p_{2,1} = 1-p_{2,2}\). Since the regime at any time is unobserved, we instead carry over time the probability of belonging to either one regime as \(\xi_{1t} + \xi_{2t} = 1\). Finally, we need to model initial values, both for returns \(r_0\) and probability of belonging to one of the two regimes \(\xi_{10}\).

In the whole, our regime-switching model is defined by the likelihood

where \(\eta_{jt} = p_{j,1}\), \(\mathcal{N}(r_t;\alpha_1, \sigma_1^2) + p_{j,2}\), and \(\mathcal{N}(r_t; \alpha_2 + \rho r_{t-1}, \sigma_2^2)\) for \(j\in\{0, 1\}\). And the priors of the parameters are:

where \(\mathcal{N}^0\) indicates the truncated at 0 Gaussian distribution and \(\mathcal{C}^+\) the half-Cauchy distribution.

Show code cell content

Hide code cell content

import matplotlib.pyplot as plt

import arviz as az

plt.rcParams["axes.spines.right"] = False

plt.rcParams["axes.spines.top"] = False

az.rcParams["plot.max_subplots"] = 50

import jax

from datetime import date

rng_key = jax.random.key(int(date.today().strftime("%Y%m%d")))

import jax.numpy as jnp

import numpy as np

import numpyro

import numpyro.distributions as distrib

import pandas as pd

from jax.scipy.stats import norm

from numpyro.diagnostics import print_summary

from numpyro.infer.util import initialize_model

import blackjax

class RegimeMixtureDistribution(distrib.Distribution):

arg_constraints = {

"alpha": distrib.constraints.real,

"rho": distrib.constraints.positive,

"sigma": distrib.constraints.positive,

"p": distrib.constraints.interval(0, 1),

"xi_0": distrib.constraints.interval(0, 1),

"y_0": distrib.constraints.real,

"T": distrib.constraints.positive_integer,

}

support = distrib.constraints.real

def __init__(self, alpha, rho, sigma, p, xi_0, y_0, T, validate_args=True):

self.alpha, self.rho, self.sigma, self.p, self.xi_0, self.y_0, self.T = (

alpha,

rho,

sigma,

p,

xi_0,

y_0,

T,

)

super().__init__(event_shape=(T,), validate_args=validate_args)

def log_prob(self, value):

def obs_t(carry, y):

y_prev, xi_1 = carry

eta_1 = norm.pdf(y, loc=self.alpha[0], scale=self.sigma[0])

eta_2 = norm.pdf(

y, loc=self.alpha[1] + y_prev * self.rho, scale=self.sigma[1]

)

lik_1 = self.p[0] * eta_1 + (1 - self.p[0]) * eta_2

lik_2 = (1 - self.p[1]) * eta_1 + self.p[1] * eta_2

lik = xi_1 * lik_1 + (1 - xi_1) * lik_2

lik = jnp.clip(lik, a_min=1e-6)

return (y, xi_1 * lik_1 / lik), jnp.log(lik)

_, log_liks = jax.lax.scan(obs_t, (self.y_0, self.xi_0), value)

return jnp.sum(log_liks)

def sample(self, key, sample_shape=()):

return jnp.zeros(sample_shape + self.event_shape)

class RegimeSwitchHMM:

def __init__(self, T, y) -> None:

self.T = T

self.y = y

def model(self, y=None):

rho = numpyro.sample("rho", distrib.TruncatedNormal(1.0, 0.1, low=0.0))

alpha = numpyro.sample("alpha", distrib.Normal(0.0, 0.1).expand([2]))

sigma = numpyro.sample("sigma", distrib.HalfCauchy(1.0).expand([2]))

p = numpyro.sample("p", distrib.Beta(10.0, 2.0).expand([2]))

xi_0 = numpyro.sample("xi_0", distrib.Beta(2.0, 2.0))

y_0 = numpyro.sample("y_0", distrib.Normal(0.0, 1.0))

numpyro.sample(

"obs",

RegimeMixtureDistribution(alpha, rho, sigma, p, xi_0, y_0, self.T),

obs=y,

)

def initialize_model(self, rng_key, n_chain):

(init_params, *_), self.potential_fn, *_ = initialize_model(

rng_key,

self.model,

model_kwargs={"y": self.y},

dynamic_args=True,

)

kchain = jax.random.split(rng_key, n_chain)

flat, unravel_fn = jax.flatten_util.ravel_pytree(init_params)

self.init_params = jax.vmap(

lambda k: unravel_fn(jax.random.normal(k, flat.shape))

)(kchain)

self.init_params = {

name: 1.0 + value if name in ["p", "sigma"] else value

for name, value in self.init_params.items()

}

# self.init_params = {name: 3. + value if name in ['sigma'] else value for name, value in self.init_params.items()}

def logdensity_fn(self, params):

return -self.potential_fn(self.y)(params)

def inference_loop(rng, init_state, kernel, n_iter):

keys = jax.random.split(rng, n_iter)

def step(state, key):

state, info = kernel(key, state)

return state, (state, info)

_, (states, info) = jax.lax.scan(step, init_state, keys)

return states, info

url = "https://raw.githubusercontent.com/blackjax-devs/blackjax/main/docs/examples/data/google.csv"

data = pd.read_csv(url)

y = data["dl_ac"].values * 100

T, _ = data.shape

dist = RegimeSwitchHMM(T, y)

n_chain, n_warm, n_iter = 128, 5000, 200

# rng_key, kinit, ksam = jax.random.split(rng_key, 3)

ksam, kinit = jax.random.split(jax.random.key(0), 2)

dist.initialize_model(kinit, n_chain)

tic1 = pd.Timestamp.now()

k_warm, k_sample = jax.random.split(ksam)

warmup = blackjax.meads_adaptation(dist.logdensity_fn, n_chain)

(init_state, parameters), _ = warmup.run(k_warm, dist.init_params, n_warm)

kernel = blackjax.ghmc(dist.logdensity_fn, **parameters).step

def one_chain(k_sam, init_state):

state, info = inference_loop(k_sam, init_state, kernel, n_iter)

return state.position, info

k_sample = jax.random.split(k_sample, n_chain)

samples, infos = jax.vmap(one_chain)(k_sample, init_state)

tic2 = pd.Timestamp.now()

print("Runtime for MEADS", tic2 - tic1)

Runtime for MEADS 0 days 00:00:21.221712

print_summary(samples)

mean std median 5.0% 95.0% n_eff r_hat

alpha[0] 0.00 1.02 0.02 -1.31 1.98 nan 1304670.88

alpha[1] 0.11 1.06 0.11 -1.66 1.68 nan 1246383.25

p[0] 0.97 1.04 1.01 -0.47 2.80 nan 960787.00

p[1] 0.87 1.02 0.80 -0.68 2.51 nan 1126165.75

rho 0.04 1.07 0.01 -1.77 1.54 nan 7190896.59

sigma[0] 0.87 1.05 0.85 -0.42 3.06 nan 1038846.31

sigma[1] 0.99 1.01 1.05 -0.78 2.47 nan 981399.00

xi_0 -0.08 1.09 -0.15 -1.64 1.88 nan 7210323.84

y_0 0.04 0.99 0.05 -1.67 1.47 nan 7626618.49

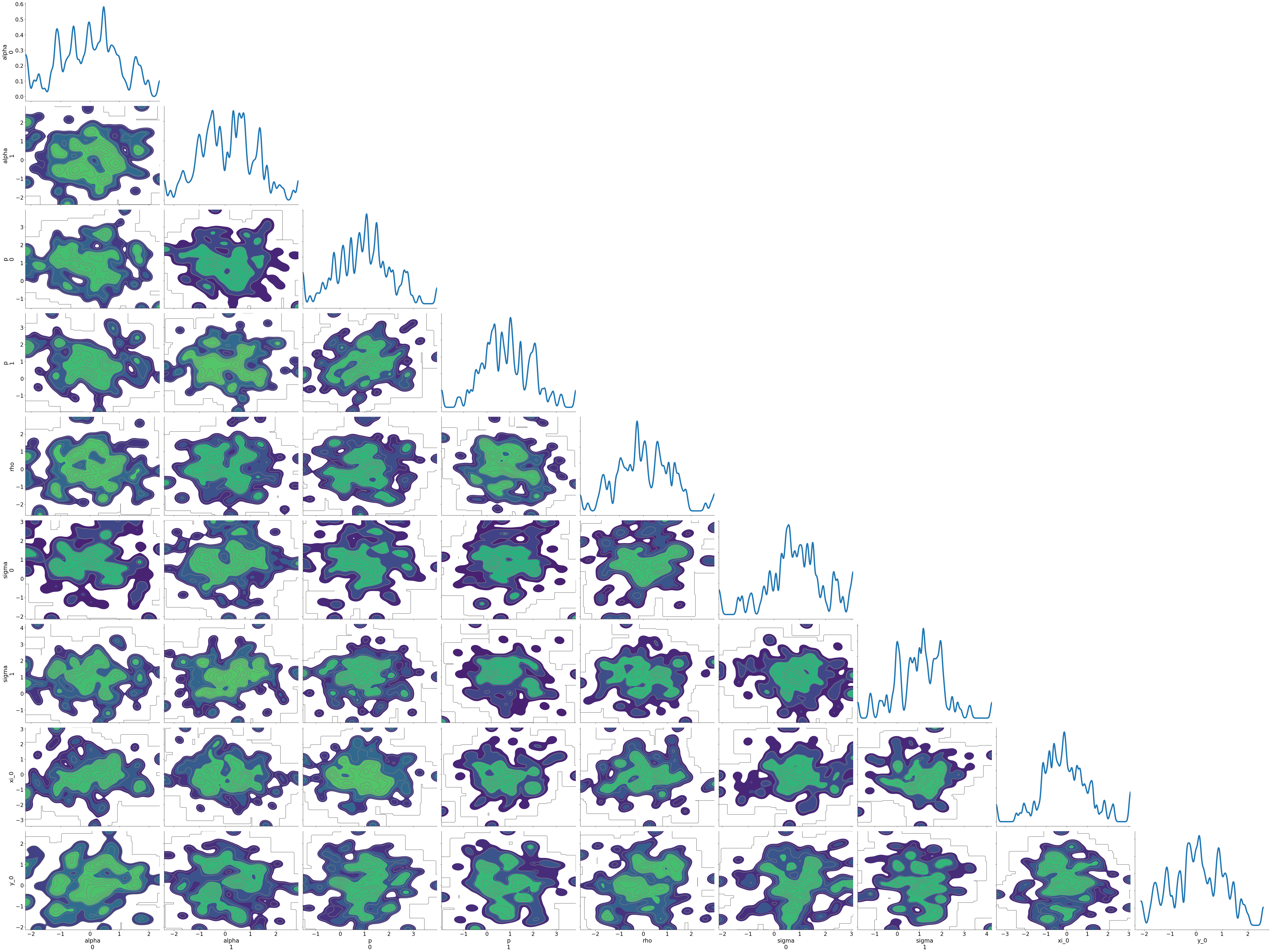

import arviz as az

idata = az.from_dict(posterior=samples)

az.plot_pair(idata, kind='kde', marginals=True, textsize=20,

marginal_kwargs=dict(plot_kwargs={"lw":5}))

plt.tight_layout();